When the team at Upptec analyses which products may develop into future claim problems, we try to identify trends early to fully understand the technology and to ensure the right data is in place when claims start being reported. In these analyses, three factors appear over and over.

The first is a new price large enough to exceed deductibles even after depreciation of two to three years, which often amounts to around 40–60%. The second is market penetration, how large a share of the population owns the product. The third is mobility, meaning the product follows the policyholder in daily life, in a pocket, bag, or directly on the body.* Products that meet two of these criteria often appear in claims. Those that meet all three almost always become high frequency items. They get dropped, forgotten or stolen. This is precisely why wearables have become an increasingly relevant category from a claims perspective.

The Smartwatch

The wearables concept really took off when Apple and Samsung launched their smartwatches in 2014. At the time, the question was whether they even had a place in a world where smartphones already fulfilled most functions. Ten years later, the answer is clear: in 2025, the number of smartwatch users in Europe was estimated at around 140–190 million people, which is roughly one-fifth of the population.

Share of the population using smartwatches by country – GWI, January 2023.

*In the Nordic countries this issue is significantly larger because home insurance often covers items even outside the home, an interpretation that is less common in the rest of Europe.

The Smart ring

However, the smartwatch is no longer alone. In recent years smart rings have also established themselves as a new wearable category. The segment was popularized in the Nordics by the Finnish company ŌURA, which by mid-2025 had sold more than five million rings globally and about half of them in the previous twelve months.

“ŌURA has sold over 2.5 million rings since June 2024, reaching in just over a year what previously took the company eleven years to achieve.” – Tom Hale, CEO ŌURA

Average new prices in actual claims in Sweden (SEK)

| Year | Headphones | Smart watch | Sportwatch | Smart ring | Smart glasses |

| 2025 | 2420 | 4424 | 5116 | 4003 | – |

| 2026 | 2353 | 4307 | 6004 | 4135 | 5236 |

The smart rings that have come through Upptec’s system in recent years have had an average new price that at times exceeded that of the smartwatches. The combination of high price and small physical size makes the smart ring a product with obvious claim potential. It’s easy to misplace and difficult to notice when it’s gone. Insurance companies will recall how both claim frequency and average cost increased sharply for headphones once they became true wireless with the introduction of AirPods.

So, is the smart ring the next major claims problem? – Probably not. More likely it will remain a complement rather than a replacement for the smartwatch.

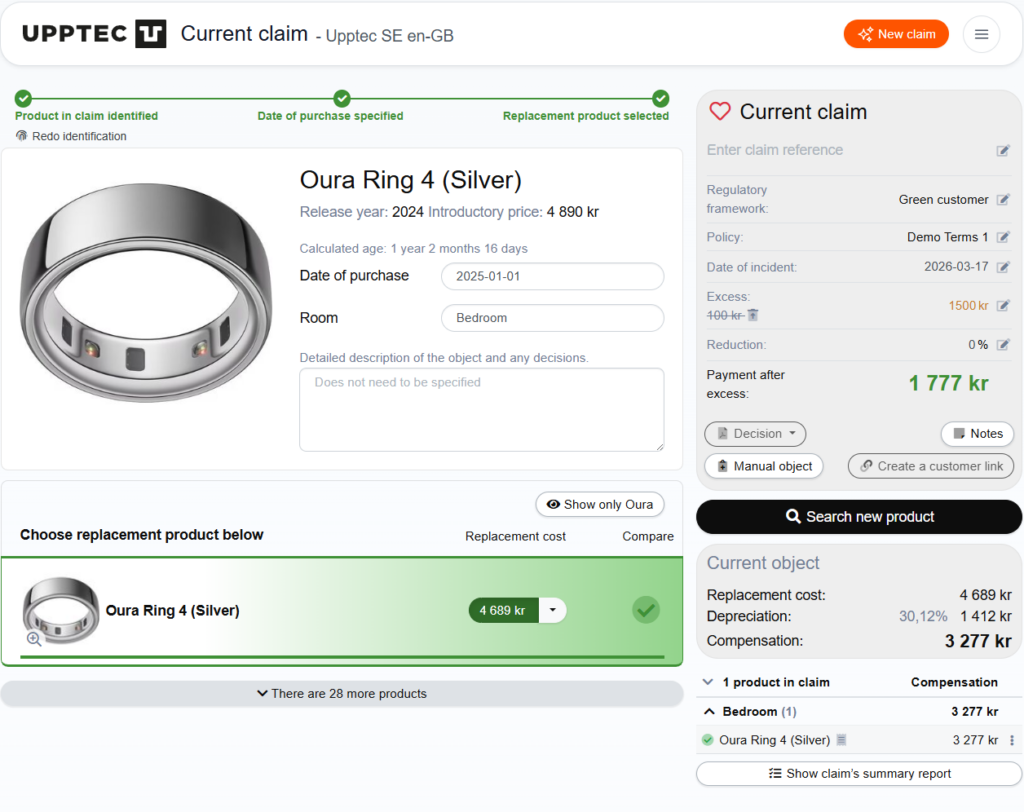

Oura ring Gen 4.

A product that appeared on the daily in Upptecs systems during February 2026.

The limited user-product interaction (often without a screen) means it mainly functions as a passive sensor rather than a back-and-forth communicating interface and market penetration will likely go nowhere near that of the smartwatch. What favours these types of passive devices and what might make them overperform in market penetration is that the application of AI functionalities are only beginning.

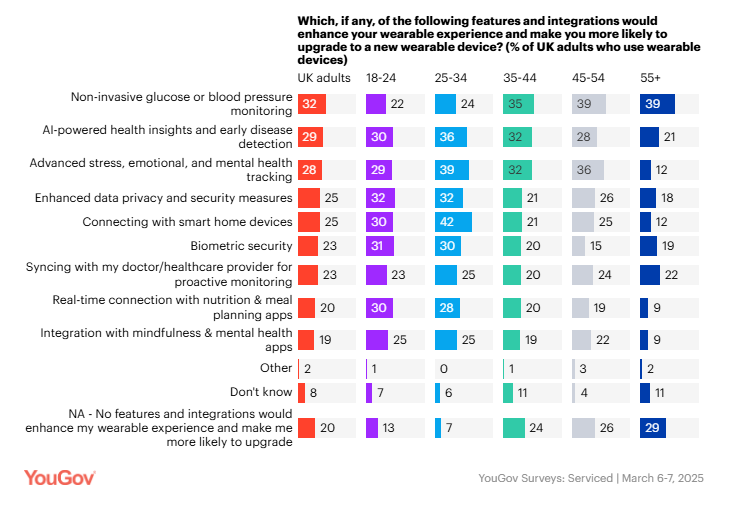

According to a YouGov study from 2025, the second most sought-after feature across all age groups was “AI-powered health insights and early disease detection,” following “Non-invasive glucose or blood pressure monitoring.” Identifying and analyzing changes in your personal baseline values could play an increasingly important role in healthcare. Imagine booking a doctor’s appointment because your ring has detected a potential health issue before you’ve even noticed any symptoms yourself.

Smart glasses

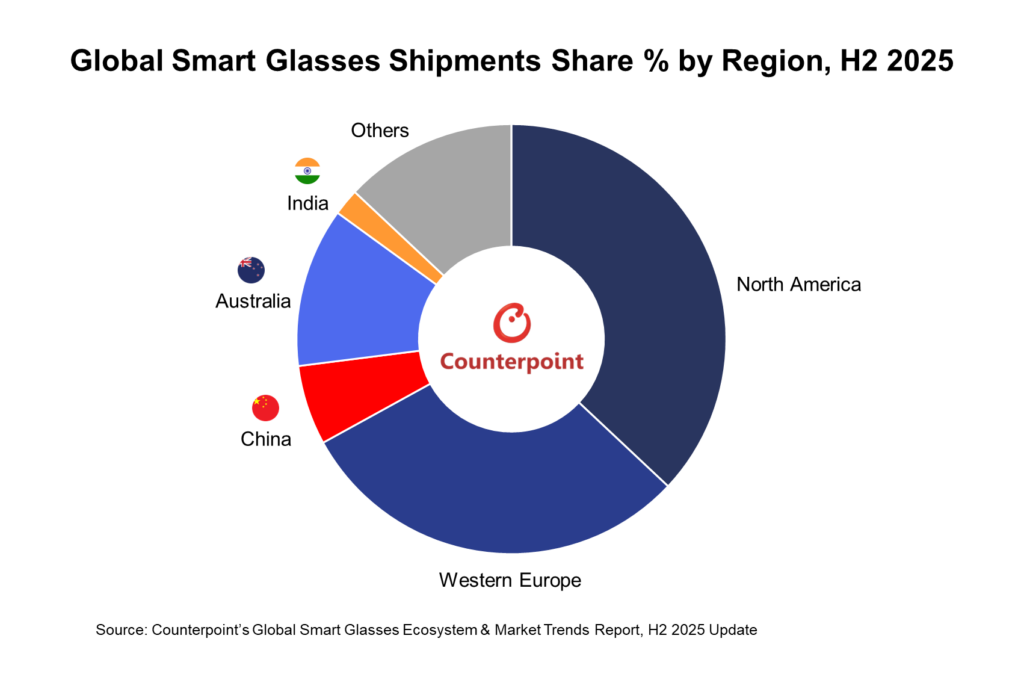

The real shift in the wearable landscape will come from the smart glasses. In an era where AI assistants can interpret speech and visual signals, the possibility opens up for glasses that listen and understand their surroundings, presenting information directly in the user’s field of vision. While smartwatches became a smartphone complement, smart glasses have the potential to become an alternative, standalone interface. The sales growth in 2025 came almost exclusively from glasses with AI functionality and 88% of the smart glasses shipped in the second half of 2025 were of this type.

counterpoint research

Signs that the category is moving beyond the experimental phase are already visible in sales figures. During 2025, seven million smart glasses were sold from Meta’s Ray-Ban series, more than three times the combined sales of the two previous years. At the same time, the global smart-glasses market grew by more than 110% during the first half of 2025. Counterpoint reports that 30% of the smart glasses shipped in the second half of 2025 were delivered to Europe.

Price: 3,000 – 7,000 SEK

Market: 7 million units sold in 2025

Growth: +110% in the first half of 2025

Market leader: Meta (~60 % market share)

Meta controlled roughly 60% of the AI smart-glasses market, but competition is expected to increase rapidly. Both Google and Samsung are developing their own models expected to launch in the coming years and CAGR is estimated to land at around 60% until 2030.

Conclusion

What does this mean for insurance providers? This is a product category with several risk factors.

Firstly, it shares many claim characteristics with other wearables: they are dropped, forgotten or lost. Like wireless headphones or traditional glasses, they are easy to leave behind at restaurants, gyms or on public transport. Secondly, they are relatively expensive consumer products, often priced at around 3,000–7,000 SEK, which (Duplantis style) easily goes over and above most depreciations and deductibles. But perhaps the most interesting aspect is that smart glasses combine two already highly claim-prone product categories in the same object: Consumer electronics + optics

The electronics parts include a camera, microphones, speakers, and a battery. Components that can easily break and require costly repairs. At the same time, glasses as a product category have traditionally had a high damage rate, as they are easily dropped, scratched or sat on. The result is a product where electronics and optics are affected in the same combined claim incidents, which can both increase the frequency of damage and make each claim all the more complex to handle.

If smart glasses follow the same adoption curve as smartwatches and wireless headphones, they will be worn by millions of people across Europe within a few years. For the insurance industry, this doesn’t just represent a new gadget, it introduces an entirely new type of claim; A new, expensive product with growing market penetration and high mobility that is also inherently fragile.

Insurance companies that want to stay ahead of the problem has to start considering solutions already.

- Should smart glasses be covered under the same terms as other home electronics?

- Are special deductibles or faster depreciations needed?

- Is there a need for specialized repair partners that have dual-capabilities in handling both electronics and optics in the same claim?

Traditionally, claim costs have to increase before insurers recognise the problem and can adapt. This is largely because many still forecast claims patterns based on historical data, which can’t capture new consumer behaviors and the claims that eventually follow. Even though insurers almost always have years of a head start as a new technology has to first enter the market, become established in the homes of their insured and then fulfill some of the factors mentioned at the start of the article. Products such as electric bikes, Hövding helmets, e-scooters and drones now have specific insurance policy rules in many of the Nordic insurers, but these were all constructed after claim costs had already risen and the new problem presented itself.

Smart glasses represent an unusually obvious risk and there is significant opportunity to avoid large claim-cost increases by adapting early. Changes that will be part of the new standard practice within a few years anyway.

2026-03-17